When it comes to planning for retirement, choosing the right Individual Retirement Account (IRA) can make a significant difference in your financial future. Two of the most popular options are the Traditional IRA and the Roth IRA. While both are designed to help individuals save for retirement, they differ in terms of tax advantages, contribution rules, and withdrawal strategies. Understanding these differences is crucial in determining which option aligns best with your financial goals and current circumstances.

The debate between Traditional IRA vs Roth IRA is not just about taxes—it’s about strategy, timing, and long-term planning. Each type of IRA has unique benefits that cater to different financial situations, making the choice highly individualistic. Whether you’re aiming to reduce your taxable income today or prefer to enjoy tax-free withdrawals in retirement, understanding how each IRA works will empower you to make an informed decision.

In this comprehensive guide, we’ll break down everything you need to know about Traditional IRA vs Roth IRA, including their key differences, eligibility requirements, tax implications, and much more. By the end of this article, you’ll gain a clearer perspective on which account might be the best fit for your retirement savings strategy.

Table of Contents

- What is a Traditional IRA?

- What is a Roth IRA?

- How Do the Tax Benefits Differ in Traditional IRA vs Roth IRA?

- Who is Eligible to Contribute to Each Account?

- What Are the Contribution Limits in 2023?

- How Do Withdrawal Rules Compare?

- Traditional IRA vs Roth IRA: Which is Better for Young Investors?

- Is It Possible to Have Both Types of Accounts?

- What Happens During Retirement?

- Traditional IRA vs Roth IRA for High-Income Earners

- How to Decide Between Traditional IRA and Roth IRA?

- Can You Convert a Traditional IRA to a Roth IRA?

- What Are the Penalties for Early Withdrawals?

- Impact of Traditional IRA vs Roth IRA on Estate Planning

- Frequently Asked Questions About Traditional IRA vs Roth IRA

What is a Traditional IRA?

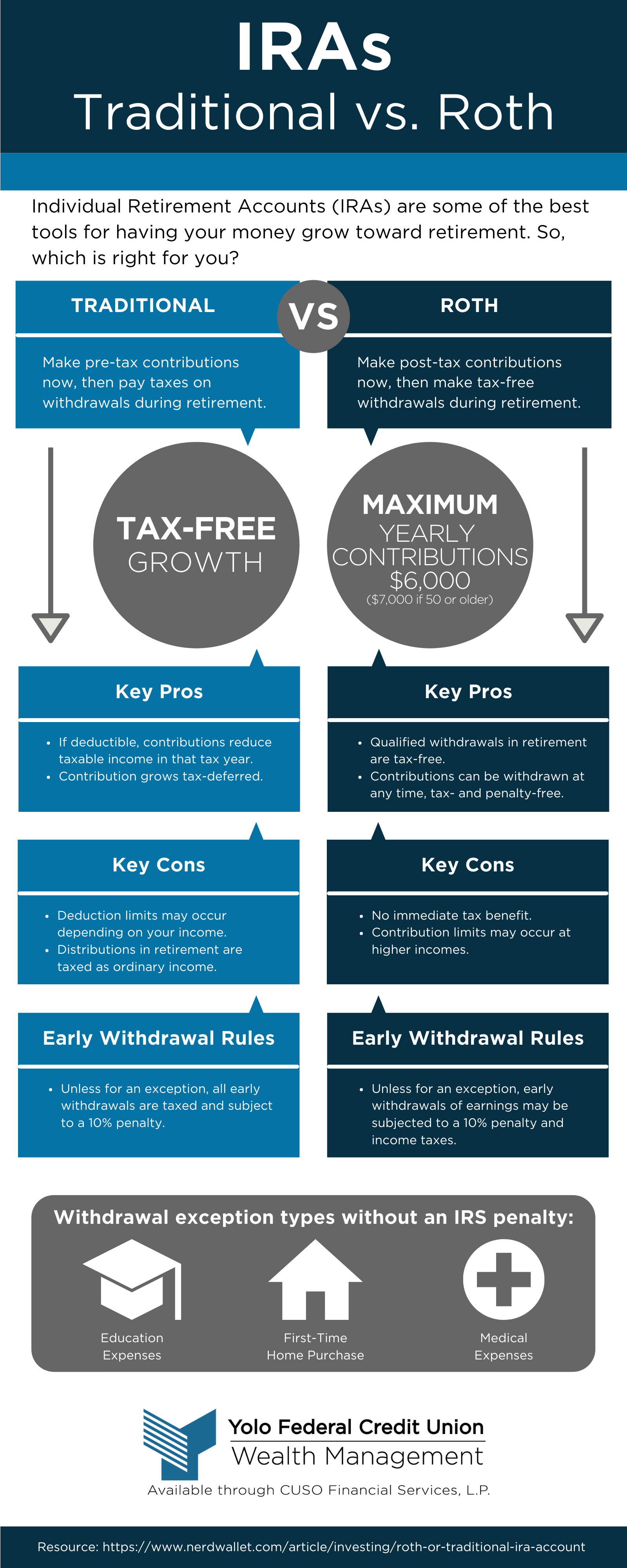

A Traditional IRA is a tax-advantaged retirement savings account that allows individuals to contribute pre-tax income, reducing their taxable income for the year. The money in the account grows tax-deferred, meaning you won't pay taxes on earnings until you withdraw them during retirement. This type of IRA is especially attractive to individuals looking to lower their current tax liability while building a nest egg for the future.

Key features of a Traditional IRA include:

- Pre-tax contributions (for those eligible).

- Tax-deferred growth on investments.

- Mandatory Required Minimum Distributions (RMDs) starting at age 73 (as of 2023).

What is a Roth IRA?

A Roth IRA, on the other hand, is funded with after-tax dollars, meaning you don’t get a tax deduction for your contributions. However, the major advantage of a Roth IRA is that qualified withdrawals during retirement are completely tax-free. This makes it an excellent option for individuals who expect to be in a higher tax bracket in the future.

Key features of a Roth IRA include:

- After-tax contributions.

- Tax-free growth and qualified withdrawals.

- No Required Minimum Distributions (RMDs) during the account holder’s lifetime.

How Do the Tax Benefits Differ in Traditional IRA vs Roth IRA?

The primary difference between the two types of IRAs lies in when you receive the tax advantage:

- Traditional IRA: Contributions are tax-deductible (if eligible), but withdrawals during retirement are taxed as ordinary income.

- Roth IRA: Contributions are not tax-deductible, but qualified withdrawals in retirement are tax-free.

Understanding your current tax bracket and expected tax rate during retirement is crucial in deciding between the two.

Who is Eligible to Contribute to Each Account?

Eligibility requirements for Traditional and Roth IRAs differ based on income level and tax filing status:

- Traditional IRA: Anyone with earned income can contribute, but the ability to deduct contributions depends on income and participation in a workplace retirement plan.

- Roth IRA: Contributions are subject to income limits. For 2023, single filers with a Modified Adjusted Gross Income (MAGI) above $153,000 and married joint filers above $228,000 are not eligible to contribute.

What Are the Contribution Limits in 2023?

The IRS sets annual contribution limits for IRAs. As of 2023, the limits are as follows:

- Under age 50: $6,500 per year.

- Age 50 and older: $7,500 per year (includes a $1,000 catch-up contribution).

These limits apply to the total contributions made to both Traditional and Roth IRAs in a single year.

How Do Withdrawal Rules Compare?

Withdrawal rules vary significantly between Traditional and Roth IRAs:

- Traditional IRA: Withdrawals before age 59½ are subject to a 10% penalty and income tax, with some exceptions. RMDs are required starting at age 73.

- Roth IRA: Contributions can be withdrawn at any time without penalties or taxes. Earnings can be withdrawn tax-free after age 59½, provided the account has been open for at least five years.

Traditional IRA vs Roth IRA: Which is Better for Young Investors?

Young investors often prefer Roth IRAs because they are likely in a lower tax bracket now than they will be in retirement. By paying taxes upfront, they can enjoy decades of tax-free growth and withdrawals.

Is It Possible to Have Both Types of Accounts?

Yes, it is possible to contribute to both a Traditional IRA and a Roth IRA in the same year, as long as your total contributions do not exceed the annual limit. This strategy allows for diversification of tax advantages.

What Happens During Retirement?

During retirement, the choice between a Traditional IRA and Roth IRA affects your tax obligations and withdrawal flexibility. Understanding the implications of each account can help you manage your income and taxes efficiently.

Traditional IRA vs Roth IRA for High-Income Earners

High-income earners often face limitations when contributing to Roth IRAs due to income caps. However, they can still contribute to a Traditional IRA or consider a backdoor Roth IRA strategy.

How to Decide Between Traditional IRA and Roth IRA?

Deciding between a Traditional IRA and Roth IRA involves evaluating your current and future tax situation, income level, and retirement goals. Consulting with a financial advisor can offer personalized guidance.

Can You Convert a Traditional IRA to a Roth IRA?

Yes, you can convert a Traditional IRA to a Roth IRA through a process known as a Roth conversion. This strategy can be advantageous if you anticipate being in a higher tax bracket in the future.

What Are the Penalties for Early Withdrawals?

Both Traditional and Roth IRAs impose penalties for early withdrawals, but the rules differ. Understanding these penalties can help you avoid unnecessary costs and maximize your savings.

Impact of Traditional IRA vs Roth IRA on Estate Planning

Roth IRAs are often favored for estate planning because they do not require RMDs, allowing the account to grow tax-free for heirs. Traditional IRAs, however, have mandatory distributions that can impact estate planning strategies.

Frequently Asked Questions About Traditional IRA vs Roth IRA

Still have questions? This section addresses common concerns and scenarios to help you make an informed decision about your retirement savings.

You Might Also Like

The Ultimate Guide To The Best Fishing Areas Around The WorldBest Horror Movies 2023: Your Ultimate Guide To Spine-Chilling Cinema

Is Dark Chocolate Good For You? Exploring Health Benefits And Myths

The Enchantment Of Fantasy Characters With Staffs: A Magical Journey

The Ultimate Guide To Finding The Best Italian Food Near Me

Article Recommendations