When it comes to financing higher education, understanding the nuances of student loan options is essential. Two of the most common types of federal student loans are subsidized and unsubsidized loans, both offered through the U.S. Department of Education. While they may seem similar on the surface, there are significant differences between them that can impact your repayment plan, interest accumulation, and overall financial health. Knowing which loan type aligns with your needs can save you from unnecessary financial stress in the future.

In the broader conversation of subsidized vs unsubsidized loans, understanding their unique features is vital. Subsidized loans are designed to provide relief to students with financial need, as the government covers the interest while you're in school at least half-time. On the other hand, unsubsidized loans accrue interest from the moment they are disbursed, regardless of your enrollment status. These differences make it crucial to carefully evaluate your options before borrowing.

In this detailed guide, we’ll explore everything you need to know about subsidized vs unsubsidized loans. From their eligibility requirements and interest rates to repayment terms and pros and cons, this article will help you make an informed decision. Whether you’re a student preparing for college or a parent helping your child navigate financial aid, this comprehensive breakdown will provide you with the clarity you need.

Table of Contents

- What Are Subsidized Loans?

- What Are Unsubsidized Loans?

- How Do Subsidized Loans Work?

- How Do Unsubsidized Loans Work?

- Who Is Eligible for Subsidized vs Unsubsidized Loans?

- What Are the Interest Rates for Subsidized vs Unsubsidized Loans?

- What Are the Repayment Options for Subsidized vs Unsubsidized Loans?

- Pros and Cons of Subsidized vs Unsubsidized Loans

- How Do These Loans Affect Your Credit Score?

- What Are the Borrowing Limits for Subsidized and Unsubsidized Loans?

- Can Subsidized or Unsubsidized Loans Be Forgiven?

- Are Subsidized Loans Available for Graduate Students?

- Tips for Choosing Between Subsidized and Unsubsidized Loans

- What Are the Alternatives to Subsidized and Unsubsidized Loans?

- Final Thoughts on Subsidized vs Unsubsidized Loans

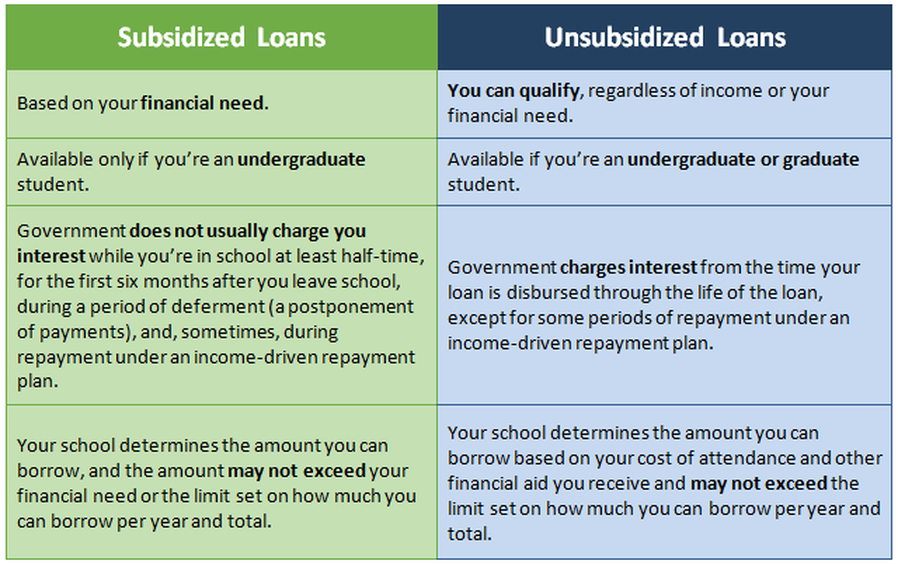

What Are Subsidized Loans?

Subsidized loans are a type of federal student loan available to undergraduate students with demonstrated financial need. These loans are unique because the U.S. Department of Education pays the interest while you’re in school at least half-time, during your grace period, and during deferment periods. This feature can significantly reduce the total cost of borrowing over time.

What Are Unsubsidized Loans?

Unlike subsidized loans, unsubsidized loans are available to both undergraduate and graduate students regardless of financial need. The primary difference is that interest begins accruing immediately upon disbursement and continues throughout the life of the loan, including while you’re in school and during deferment periods. This makes unsubsidized loans a more expensive option in the long run.

How Do Subsidized Loans Work?

Subsidized loans are designed to provide financial relief to students who qualify based on need. The government covers the interest during specific periods, making them a cost-effective way to fund your education. Here’s how they work:

- Eligibility is determined by your FAFSA (Free Application for Federal Student Aid) submission.

- Interest is paid by the government while you’re in school at least half-time.

- You have a six-month grace period after graduation before repayment begins.

How Do Unsubsidized Loans Work?

Unsubsidized loans are accessible to a broader range of students but come with fewer benefits. Here’s a breakdown of how they function:

- No financial need requirement for eligibility.

- Interest starts accruing from the moment the loan is disbursed.

- You can choose to pay interest while in school or allow it to capitalize, increasing the total loan amount.

Who Is Eligible for Subsidized vs Unsubsidized Loans?

Eligibility requirements differ significantly between subsidized and unsubsidized loans:

- Subsidized Loans: Reserved for undergraduate students with financial need. Eligibility is determined based on FAFSA results.

- Unsubsidized Loans: Available to undergraduate, graduate, and professional students regardless of financial need.

What Are the Interest Rates for Subsidized vs Unsubsidized Loans?

Interest rates for federal student loans are set by Congress and can vary annually. As of the most recent update:

- Subsidized Loans: Typically have a lower interest rate compared to unsubsidized loans.

- Unsubsidized Loans: Interest rates are usually higher, especially for graduate and professional students.

What Are the Repayment Options for Subsidized vs Unsubsidized Loans?

Both loan types offer a variety of repayment plans to accommodate different financial situations. These include:

- Standard Repayment Plan

- Graduated Repayment Plan

- Income-Driven Repayment Plans

Pros and Cons of Subsidized vs Unsubsidized Loans

Understanding the advantages and disadvantages of each loan type can help you make a more informed decision:

- Subsidized Loans Pros: No interest accrual during school, lower overall cost.

- Subsidized Loans Cons: Limited to undergraduate students, borrowing limits may be lower.

- Unsubsidized Loans Pros: Available to all students, higher borrowing limits.

- Unsubsidized Loans Cons: Interest accrues immediately, increasing the total cost.

How Do These Loans Affect Your Credit Score?

Timely repayment of both subsidized and unsubsidized loans can positively impact your credit score. However, defaulting or missing payments can have severe consequences on your creditworthiness.

What Are the Borrowing Limits for Subsidized and Unsubsidized Loans?

Federal student loans have annual and aggregate borrowing limits. Subsidized loans generally have lower limits compared to unsubsidized loans. For example:

- Dependent undergraduate students: Up to $31,000 (no more than $23,000 in subsidized loans).

- Independent undergraduate students: Up to $57,500 (no more than $23,000 in subsidized loans).

Can Subsidized or Unsubsidized Loans Be Forgiven?

Both loan types may qualify for federal loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness. However, eligibility depends on your career path and repayment plan.

Are Subsidized Loans Available for Graduate Students?

Unfortunately, subsidized loans are not available for graduate or professional students. Graduate students can only access unsubsidized loans or alternative funding options.

Tips for Choosing Between Subsidized and Unsubsidized Loans

Here are some tips to help you decide:

- Start with subsidized loans if you qualify, as they are more cost-effective.

- Borrow only what you need to cover educational expenses.

- Consider making interest payments on unsubsidized loans while in school to reduce overall debt.

What Are the Alternatives to Subsidized and Unsubsidized Loans?

Other options include:

- Scholarships and grants

- Work-study programs

- Private student loans (use with caution)

Final Thoughts on Subsidized vs Unsubsidized Loans

Understanding the key differences between subsidized and unsubsidized loans is crucial for making informed financial decisions. While subsidized loans offer significant advantages for those who qualify, unsubsidized loans can provide additional funding when needed. Carefully consider your financial situation, future earning potential, and repayment options before committing to any loan.

You Might Also Like

Exploring The Timeless Brilliance Of Amadeus MovieExploring The Curious Question: What Does Cum Taste Like?

Unlocking The World Of Fit Girl Repack: A Comprehensive Guide

What Is DLC Meaning? Exploring The Definition, Types, And Importance

Understanding The Importance Of The Supreme Law Of The Land

Article Recommendations

:max_bytes(150000):strip_icc()/federal-direct-loans-subsidized-vs-unsubsidized-Final-f0f41bb91a7143fbb1657b8d352c6ae7.png)